Basic Setup

%matplotlib inline

import numpy as np

from matplotlib import pyplot as plt

from numpy.random import normal

T = 2.0

n = 100

dt = T / n

First test: solving a simple equation

x = np.zeros(n + 1)

for i in xrange(n):

x[i + 1] = x[i] + dt + normal(scale = dt)

t = np.linspace(0, T, n + 1)

plt.plot(t, x, '*')

[<matplotlib.lines.Line2D at 0x3a55b10>]

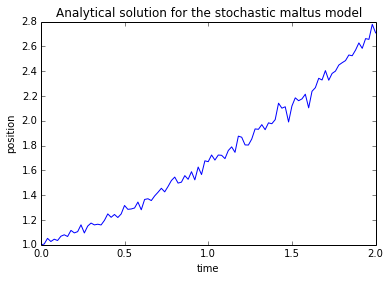

Stochastic maltus model

Problem parameters

r = 1

c = 1

x0 = 1

t = np.linspace(0, T, n + 1)

Analytic solution

factor = r - c**2 / 2.0

x = np.ones(n + 1)

w = normal(scale=dt, size=n + 1)

w[0] = 0

x = x0 * np.exp(factor * t + c * w)

plt.plot(t, x)

plt.title('Analytical solution for the stochastic maltus model')

plt.xlabel('time')

plt.ylabel('position')

<matplotlib.text.Text at 0x48dd910>

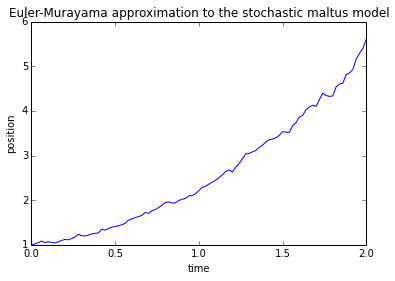

Euler-Murayama approximation

x2 = np.zeros(n + 1)

x2[0] = x0

for i in xrange(n):

xi = x2[i]

x2[i + 1] = xi + r * xi * dt + c * xi * normal(scale = dt)

plt.plot(t, x2)

plt.title('Euler-Murayama approximation to the stochastic maltus model')

plt.xlabel('time')

plt.ylabel('position')

<matplotlib.text.Text at 0x4dd5b50>

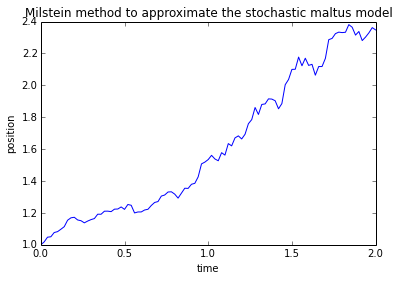

Milstein method

x3 = np.zeros(n + 1)

x3[0] = x0

for i in xrange(n):

xi = x3[i]

wi = normal(scale = dt)

x3[i + 1] = xi + r * xi * dt + c * xi * wi + 0.5 * c * xi * c * (wi**2 - dt)

plt.plot(t, x3)

plt.title('Milstein method to approximate the stochastic maltus model')

plt.xlabel('time')

plt.ylabel('position')

<matplotlib.text.Text at 0x4dcc590>

Qualitative comparison

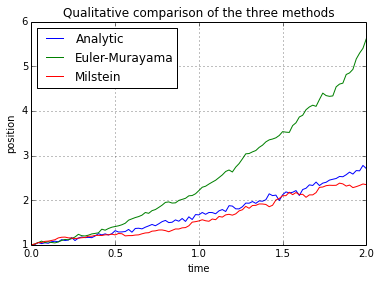

plt.plot(t, x, t, x2, t, x3)

plt.title('Qualitative comparison of the three methods')

plt.xlabel('time')

plt.ylabel('position')

plt.legend(('Analytic', 'Euler-Murayama', 'Milstein'), loc='upper left')

plt.grid()

As it was expected, euler’s method is more prone to error than Milstein’s correction. It remains to make a comparison of results for different values of the parameters. It is not expected any important difference in the results if varying initial conditions

Appendix: Routines for solving sde

It is straightforward to write routines for solving stochastic equations with Euler-Murayama’s and Milstein’s methods. For later, convenience, they are written here.

def emurayama(T, timesteps, x0, alpha, beta):

'''

x = emurayama(T, timesteps, x0, alpha, beta)

solves the stochastic differential equation

dx = alpha * dt + beta * dw

x(0) = x0

with Euler-Murayama method.

input:

T = Final time.

timesteps = Number of timesteps to use.

x0 = initial condition.

alpha, beta = equation parameters. Must be functions like this:

x = alpha(xi, ti),

i.e. its input must be two floating point numbers and must return another floating point.

(No vectorization, due to the recursive definition of the algorithm)

returns:

array of lenght timesteps + 1 with the result.

'''

x = np.zeros(timesteps + 1)

x[0] = x0

ti = 0.0

dt = float(T) / timesteps

for i in xrange(timesteps):

xi = x[i]

ti += dt

x[i + 1] = xi + alpha(xi, ti) * dt + beta(xi, ti) * normal(scale = dt)

return x

def milstein(T, timesteps, x0, alpha, beta, diff_beta):

'''

x = milstein(T, timesteps, x0, alpha, beta)

solves the stochastic differential equation

dx = alpha * dt + beta * dw

x(0) = x0

with Milstein's method.

input:

T = Final time.

timesteps = Number of timesteps to use.

x0 = initial condition.

alpha, beta = equation parameters. Must be functions like this:

x = alpha(xi, ti),

i.e. its input must be two floating point numbers and must return another floating point.

(No vectorization, due to the recursive definition of the algorithm)

diff_beta = partial derivative of beta, respect to x.

returns:

array of lenght timesteps + 1 with the result.

'''

x = np.zeros(timesteps + 1)

x[0] = x0

ti = 0.0

dt = float(T) / timesteps

for i in xrange(timesteps):

xi = x[i]

ti += dt

wi = normal(scale = dt)

x[i + 1] = xi + alpha(xi, ti) * dt + beta(xi, ti) * wi + 0.5 * beta(xi, ti) * diff_beta(xi, ti) * (wi**2 - dt)

return x